Key takeaways

|

While those of us in the nursing profession adapt easily to rapid clinical changes and frequent updates in electronic data-management systems, many of us cringe when it comes to learning the nuances of healthcare finance. But as we enter management positions, we’re often responsible for developing expense, revenue, and capital budgets; justifying variances; and flexing personnel and supplies to achieve budget targets. In addition, a new generation of advanced practice nurses are pursuing independent practice options. In other words, they’re becoming small business owners who need to understand healthcare finance.

Meaning behind the terms

The best place to start is by developing an appreciation for the common terms that underpin most financial conversations in healthcare, which facilitates discussion and data exchange.

• Usefulness for decision making refers to the relevance and consistency of information, which ensures accuracy and availability for immediate use.

• Information should contain data that is verifiable and reproducible when subjected to multiple calculations.

• Usefulness requires that information be available in a timely fashion and in a format understood by all parties so that data can be compared.

Financial statements

Financial statements contain elements defined by their usefulness for decision making and ability to be verified, reproduced, and compared. The most common types of financial statements are the statement of revenue and expenses, the statement of net worth, the statement of cash flow, and the balance sheet.

• Statement of revenue and expenses primarily results from the following formula:

Operating revenue – Operating expense = Operating income

Details for each portion of the formula provide necessary information for interpreting bottom-line operational performance.

• Statement of net worth reflects the following:

Assets – Liabilities = Net worth

This formula creates an overview of the value of a business, such as a hospital, a hospital system, or a freestanding clinical practice.

• Statement of cash flow contains a summary of the actual or anticipated cash income or expenses for a specific period of time, such as monthly, quarterly, or annually.

• Balance sheet records what an organization owns, what it owes, and what it’s worth. Experts view the balance sheet as a snapshot that freezes the figures and reports them as of a certain date. It balances assets, liabilities, and net worth.

Financial statements usually contain commonly accepted financial terms. Understanding these basic terms makes it easier for you to have meaningful discussions with financial and business experts.

• Assets are resources—tangible or intangible—that have some value, such as consumable assets like cash or medical supplies. Fixed assets include equipment, buildings, or real estate.

• Liabilities refer to any transaction in which owed money reduces an organization’s economic benefit.

Examples are loans and any expenses that vary with volume, such as supplies.

• Equity is any money or value that remains after paying off all debts. For instance, an ambulatory practice generates $1.2 million in annual revenue, but after paying all debts, only $250,000 in equity remains. This remaining amount may fall significantly short of an owner’s original investment.

• Revenue results from receiving more money than spent when providing services or products. Arriving at revenue-accurate projections requires an in-depth understanding of healthcare costing systems such as diagnosis-related groups, relative value units, and ratio of costs to charges.

• Expenses, or the cost of doing business, represent all money spent or costs incurred in an effort to generate revenue.

• Gains and losses refer to increases in assets (gains) and conditions where liabilities exceed assets and result in losses, which are usually measured monthly, quarterly, or annually.

It’s not all unfamiliar

By now, you recognize that you may have stepped into a somewhat unfamiliar environment. But some financial terms will be familiar to nurse managers, including fiscal year, operating and capital budgets, costs and cost variances, overhead, and budget variances.

• Fiscal year is a 12-month period within which businesses plan for operations, create revenue, spend money, and measure overall business performance. Fiscal years can begin and end at set points that differ from a calendar year of January 1 to December 31. For instance, many hospitals have a fiscal year that runs from July 1 to June 30.

• Operating budgets help managers administer the daily operations that feed the financial reporting process. Revenue and expense budget allocations are frequently analyzed to compare performance to budget targets or expectations. Operating budgets define several elements (for example, personnel and related expenses, such as benefits, supplies, and training) and vary depending on the business.

• Capital budgets define large purchases planned for a fiscal year, such as medical equipment, building expansions, and infrastructure replacement or improvements. Some capital purchase payments and projects extend over several fiscal years with annual capital budget carryover expenses reflected in subsequent fiscal year budgets.

• Costs refer to any expense of resources, quantified in dollars, necessary for the business to produce its product, such as healthcare services. They can be broken down into several categories: direct, indirect, fixed, variable, and semivariable. Appreciating their importance and managing them within budget parameters are key to the success or failure of any business. (See What are the costs?)

Knowledge of cost variances becomes extremely important in managing any business operation. Once constructed, the budget for a fiscal year undergoes considerable monthly scrutiny comparing anticipated volume and acuity-related revenue (revenue that varies with illness severity) with budgeted expenses. Cost overruns and general budget versus actual variances may require not only explanation, but also immediate expense reduction for a business to survive.

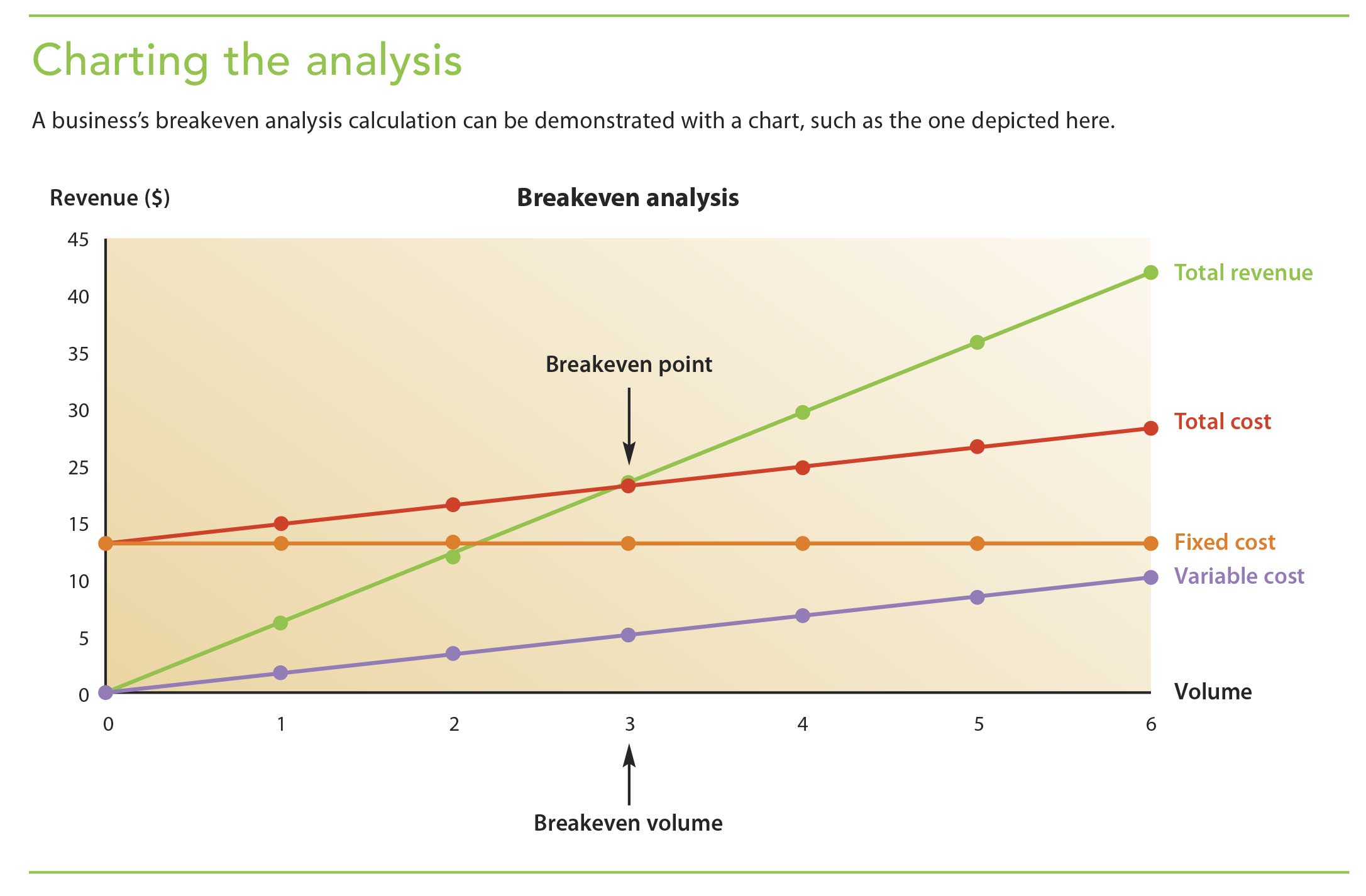

Breaking even

The breakeven analysis calculation enables a business to better understand its potential solvency. Simply put, this calculation demonstrates the point at which all revenue covers all costs. At the breakeven point, a business neither loses money nor makes a profit. Instead, it signals a profit potential that assumes revenue will continue to climb and expenses will remain stable. (See Charting the analysis.)

The language of success

Learning and embracing the language of healthcare finance enables us to quantify our contribution as nurses in the healthcare industry, and it also allows us to pursue all the business opportunities available to us. Think about that the next time you negiotate your employment contract, embark on developing an independent freestanding practice, or engage in discussions with financial experts eager to secure expense reductions. Understanding the language of healthcare finance enhances your ability to achieve success not only for nursing’s well-being and advancement, but also for the patients we serve.

Joyce E. Johnson is an associate professor at the Catholic University of America in Washington, DC.

Selected references

Baker JJ, Baker RW. Health Care Finance: Basic Tools for Nonfinancial Managers. 4th ed. Burlington, MA: Jones & Bartlett Learning; 2014.

Committee on the Robert Wood Johnson Foundation Initiative on the Future of Nursing, at the Institute of Medicine. The Future of Nursing: Leading Change, Advancing Health. Washington, DC: National Academies Press; 2010.

Harrington MK. Health Care Finance and the Mechanics of Insurance and Reimbursement. Burlington, MA: Jones & Bartlett Learning; 2016.

Paterson MA. Healthcare Finance and Financial Management: Essentials for Advanced Practice Nurses and Interdisciplinary Care Teams. Lancaster, PA: DEStech Publications; 2014.

{kind=link}

1 Comment.

This is great! We need more of this in Nursing so we can benefit from “external” expertise/perspective. Thank you for simplifying this for those of us new to healthcare finance or who need to better understand how to account for savings/ROI and manage expenses of their department/operations and/or professional organizations!